The Patented.ai Edge · Why This Campaign Starts at Day 0, Not Month 18

The Patented.ai Edge · Why This Campaign Starts at Day 0, Not Month 18

Automated collection from authoritative records: USPTO, SEC, CFTC, on-chain data, and web archives. The 6-month research phase that a 4-attorney team used to run now finishes in days.

Each finding is backed by 3–7 primary sources, reviewed by IP attorneys, and ranked by source authority before it ships. Speculative theories are cut — only evidence that survives litigation scrutiny stays in.

Complete drafts handed off: complaint, patent-eligibility (§ 101) shield brief, claim-construction (Markman) brief, and per-defendant notice letters. Counsel reviews, edits, files — no rebuilding from scratch.

Eduardo Burillo

Founder of Accretion Capital. Operator-investor in PrizePicks (sold to Allwyn Sep 2025; $1.6B upfront / up to $4.15B with performance earnout; now first DFS operator with CFTC FCM; PrizePicks Predicts launched Nov 2025 with Kalshi + Polymarket), WagerWire, StakeKings, and Hedge Kings.

Jeffrey Gross

Partner at Accretion Capital alongside Burillo — co-backer of PrizePicks. Investor in Playmaker Betting. Former senior executive at partypoker. $5M+ professional poker earnings.

Single-step assignments from inventors to owners — no third-party licenses, no security interests, no outstanding liens. Hedgekings LLC owns '965/'966; Wymond Labs LLC owns '706/'161. Both LLC principals aligned — engagement letters execute within the 6-week decision window.

Prosecution discipline: Burillo's counsel filed 5 wager-focused patent apps — all 5 cleared the eligibility bar. The 3 non-wager apps filed in parallel were rejected. Evidence of deliberate, skilled drafting.

tribal compact

8 categories

eBay injunction lever

+ NYRABets · 1/ST BET

+ NYRABets · 1/ST BET

+ Betr Picks

+ Betr Picks

") + Collectable

+ Collectable

")

")

") Stats Perform (+Opta) · Second Spectrum · Synergy

Stats Perform (+Opta) · Second Spectrum · Synergy

The industry sorted itself into two camps

★★ Judicial-Estoppel Masterstroke

FanDuel Ltd

★★ Judicial-Estoppel Masterstroke

FanDuel Ltd

FanDuel's own USPTO filings admit every '965/'161 element — including a granted patent on AI bet-recommendation — and their standalone FCM kills CFTC preemption.

(1) App 19/410,345 verbatim: "favorite teams, favorite players, favorite betting practices… user 210 may be specifically targeted" + "convolutional neural network-based model." (2) App 19/410,174 + 18/893,179: "recommending at least one alternative market" + "surfaced to a user via a graphical user interface." (3) US 12,307,861 B1 GRANTED (May 20, 2025): "bet embedding… similarity score" — LITERAL '965 E3/E4. Granted = final USPTO position.

★★ Markman Anchor · FRE 902(1)

Wire Industries Inc.

WagerWire's own abandoned USPTO filings admit the entire '965 architecture — sworn by co-founders Doctor + Dotan + Geiger.

Wire Industries App 17/938,040 + 17/938,038 Claim 1: "computerized ticket exchange system … fractional bet sale of less than 100% portion … first win amount" + Claim 2: "maintaining a first ledger at a database for tracking fractional ownership." Both abandoned after USPTO § 101 Final Rejection (2025) using verbatim Rosen language — the exact framework Burillo's 5 granted patents already cleared. Inventors Doctor (CEO) + Dotan (COO) + Geiger (CXO) = current co-founders.

7 Own-Patents + 2 SEC Filings

DraftKings · DKNG

DraftKings admits the patented architecture across nine sworn filings — two SEC filings + seven granted USPTO patents (six Inc. + one SBTech subsidiary) covering '965, '706, AND '161 — each individually binding.

(1) DKNG 10-K FY25: "We build recommendations…most likely to enter." (2) CEO Robins Q4 2025 letter: "set prices — or odds — at which they buy and sell event contracts." (3) US 11,574,522 B1: "personalized session interface…ranking…viewer player profile" = '965 E1+E2+E3. (4) US 11,622,156 B1: "meter…time remaining for the event" = '706 H4 verbatim. (5) ★ US 11,457,285 B1 "Notifications of Critical Events": "change in odds…notification generation threshold…display a notification…actionable object that, when interacted with, causes…navigate to a broadcast of the live event" — '161 N2+N4+N5+N7 literal architecture. (6) US 11,451,878 B1: profile-history-based personalized content selection = '965 E1-E3. (7) US 11,445,264 B1: wager-by-wager ledger with user-profile identifiers = '965 E5 support. (8) US 11,606,598 B2: "modifying the first display region…responsive to…wager" = '706 H4 HUD overlay. (9) ★ SBTech US 11,514,758 B2 (DK subsidiary since Apr 2020): "countdown timer…dynamically calculates the probability of a sport or game incident happening within said time period…GUI widget…animation of said defined incident" = '706 H4 countdown meter + '161 N2/N3/N6/N7 pulse-betting architecture.

★ CFTC-sworn + Peer-Reviewed

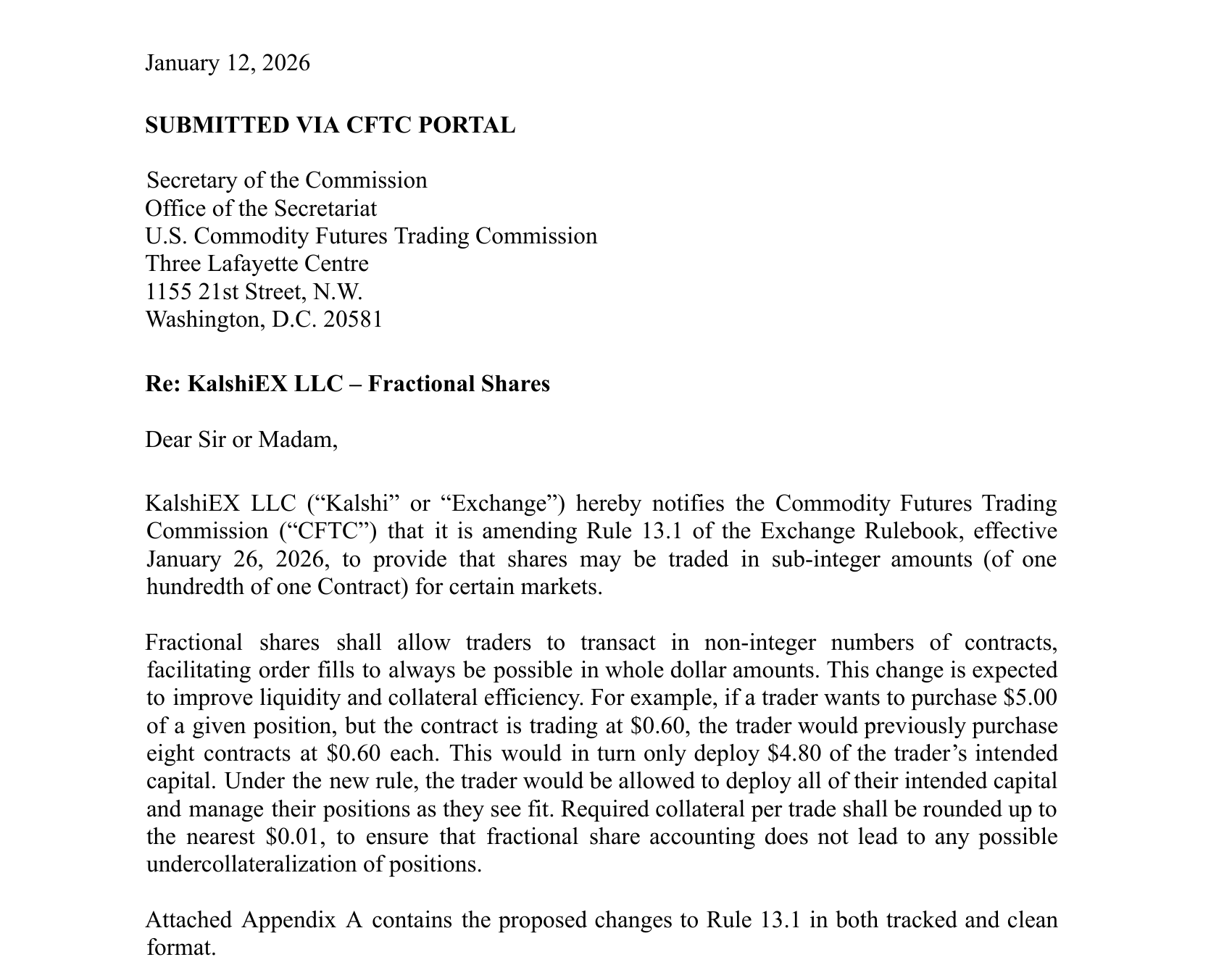

KalshiEX LLC · $22B val

Kalshi's CFTC-sworn rulebook + peer-reviewed UCD paper admit '965 E3 + E4 verbatim — the two dispositive elements.

(1) CFTC Rule 13.1(a) (Jan 12, 2026 · CRO Heaslip signature): "The minimum unit of trading is one hundredth of one Contract" — LITERAL '965 E4 fractional-locked-price construction. (2) Help Center: "every trade… between a 'maker' and a 'taker'" + API is_taker boolean — LITERAL E3 counterparty. (3) Whelan/Bürgi/Deng (UCD, Jan 2026) peer-reviewed paper with 300K-contract dataset confirms the architecture. (4) Kalshi Rulebook v1.24 (current version, updated Feb 23, 2026 · Chief Compliance Officer certified · FRE 902(1) self-authenticating) layers four additional verbatim admissions: Rule 6.7(f) requires position transfers only through the platform = '706 intra-platform resale channel · "central limit order book" (15 occurrences) = '965 aftermarket architecture · "Market Maker" (35 occurrences + dedicated Chapter 4) = '965 brokered architecture · Rule 3.1 grants each Member the right to "buy Contracts… sell Contracts… on the Platform" = '965/'966 core exchange mechanic.

★★ CEO-on-record · Markman Gift

Fanatics · FBG + Morton St.

Fanatics' own CEO defined the product as "trading" — the exact vocabulary Burillo used to distinguish his invention at the USPTO.

(1) Matt King, CEO Fanatics Betting & Gaming (Sportico Dec 3, 2025): "I look at these as trades, right?… I view this as trading." (2) CDNA Rulebook (Jan 28, 2026): "Opening Trade Value…at which the Contract is opened" + "Closing Trade Value…at which the Contract is closed" — structurally maps Burillo's 2020 odds-at-acquisition vs odds-at-exit distinction. (3) Fanatics Terms of Use: "our affiliate, Morton St. Market Maker, LLC… may provide quotes and trade in listed products on CDNA. When you trade on CDNA, your orders may be matched against Affiliate's orders" — LITERAL '965 E3 specific-counterparty. (4) Peter Jackson, FanDuel parent Flutter CEO (Sportico Feb 2026): "pricing complex correlated outcomes accurately is something we do every day… actively evaluating" — industry cross-confirmation of the affiliated-MM pattern.

★ Defendant's Own Code · Forensic

DK Predictions webapp

DK's embedded Game Tracker is supplied by Simplebet — whose own product page AND three granted patents admit the '706 HUD and '161 pre-cognizant ML architectures simultaneously.

(1) The predictions.draftkings.com webapp ships compiled JS hard-coding simpleBetUrl: "https://matchviz.simplebet.io/" + API key (live fetch Apr 21, 2026). The embedded Simplebet HTML declares <title>Game Tracker</title> + Flutter app-ID "game_tracker". (2) Simplebet's own product page (simplebet.ai/products/gametracker): "our game tracker collapses to a minimized view so fans can still follow the action while placing their bets" = LITERAL '706 C4 HUD overlay behavior. (3) Three granted Simplebet patents self-admit the '161 architecture: US 12,293,263 B2 ("predicting future outcomes in a sporting match" — N1+N2 pre-cognizant CNN); US 11,451,842 B2 ("predicting a match state event…from live multimedia" — N3+N4); US 12,015,812 (continuation of '842 — same architecture, granted Jun 18, 2024).

★ 5-in-1 Help-Center Centerpiece

Robinhood · HOOD

Robinhood's Help Center admits five elements across '965, '706, and '161 — all on a single public URL.

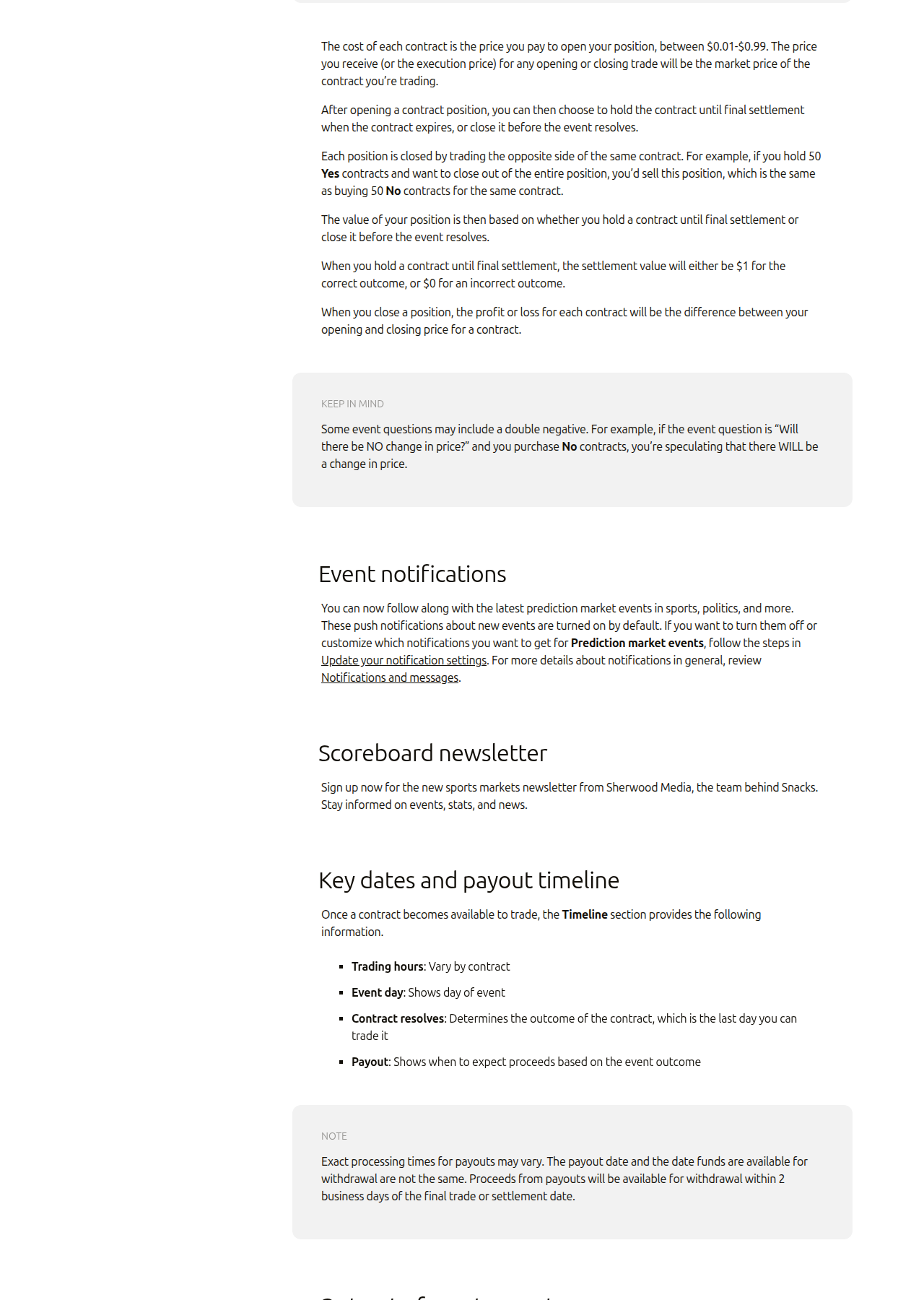

robinhood.com/…/robinhood-event-contracts: (1) "$0.01–$0.99 cost" + "$1 or $0 payout" (E4). (2) "fractional contracts… up to 2 decimal points" (E5). (3) Timeline: "Trading hours · Event day · Contract resolves · Payout" ('706). (4) "Event notifications turned on by default" ('161 push). (5) "RFQ sent to the exchange" (E3 counterparty).

Four SIG specific-intent admissions — CFO-sworn, multi-year, pre-dating — satisfy every § 271(b) element without a subpoena.

(1) RH CFO Verma, Feb 11, 2026 Q4: "Susquehanna owns 45% of the JV" — Reg-FD admission. (2) SIG SVP Pollard, Apr 3, 2024 Kalshi PR: "SIG is excited to support… providing liquidity." (3) Jeff Yass (SIG founder), Moontower Oct 31, 2025: "a great passion of ours for years." (4) Scale: Kalshi co-founder Lopes Lara Nov 2025 — internal MM "less than 6% of making volume" → SIG ≥94% of Kalshi MM.

★ § 271(b) Quadruple · Three-Patent Read

Sportradar · NASDAQ: SRAD

★ § 271(b) Quadruple · Three-Patent Read

Sportradar · NASDAQ: SRAD

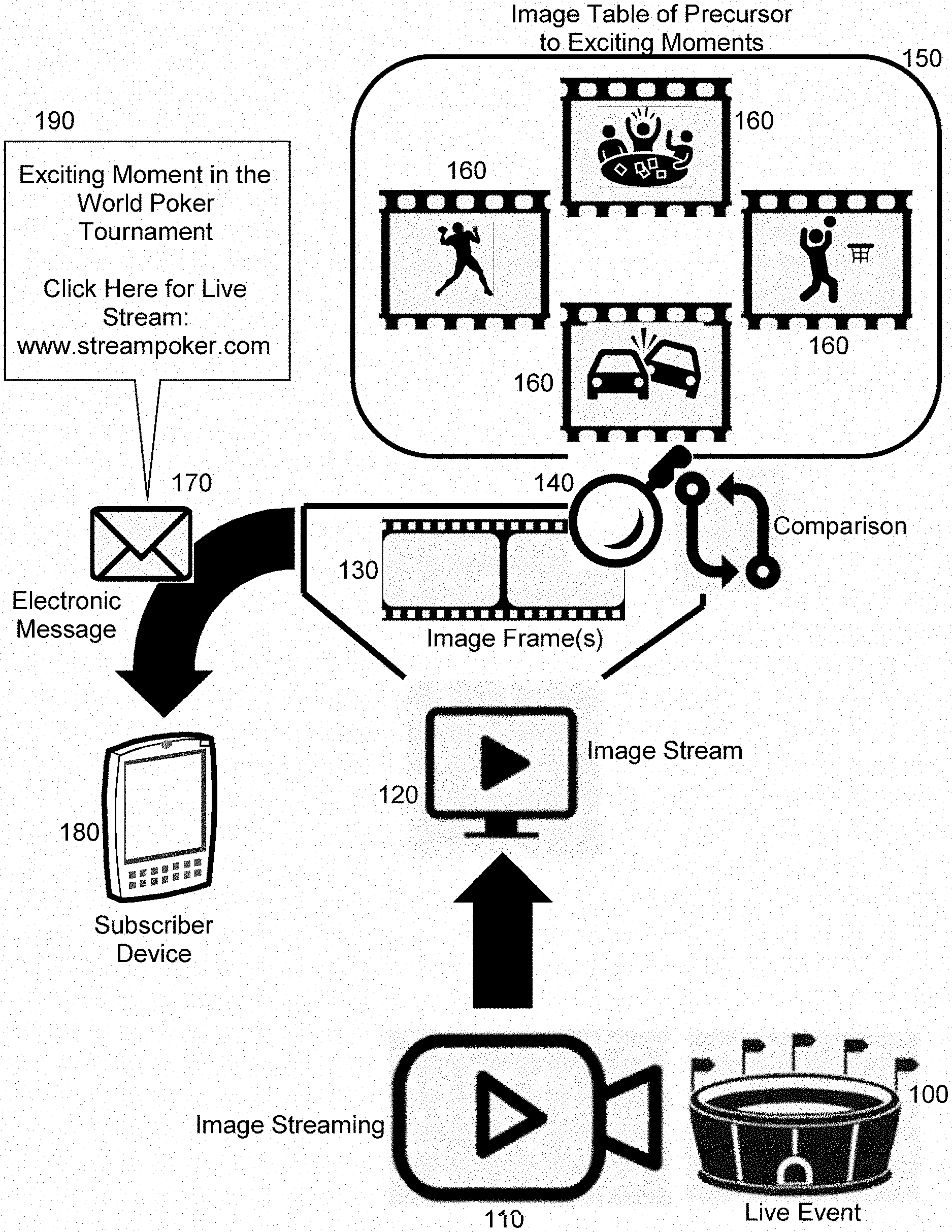

Sportradar's AWS-published soccer-goal predictor literally matches Burillo's "pre-cognizant" claim language by 2 seconds — and the 4Sight product page admits the '706 HUD architecture on its own website.

(1) AWS Soccer Goal Predictor (aws.amazon.com/blogs): "computer vision-based… predict future soccer goals 2 seconds in advance of the event" = LITERAL '161 N2 pre-cognizant. (2) Foresight basketball generative model: "trained on billions of 3D body pose data points… reads body positions in real time to predict what's likely to happen next" = '161 N1+N2 CNN. (3) 4Sight Streaming product page: "uses AI to overlay real-time stats and insights directly onto live video" = LITERAL '706 C4 HUD (100K+ events/yr served into DK/FD/ESPN/Caesars). (4) MLB Mar 19, 2026 PR: "Polymarket will also get access to Official League Data from Sportradar, MLB's exclusive global distributor of data for prediction markets" = $150-300M 3-yr exclusive gatekeeper. (5) Koerl CEO Q4 '25 earnings: "we have the ability to power this market end-to-end… monetize this opportunity" — SEC-filed FRE 801(d)(2)(D) specific-intent.

★ § 271(a) Direct · SOX-Certified

Webull · NASDAQ: BULL

★ § 271(a) Direct · SOX-Certified

Webull · NASDAQ: BULL

Webull's Vega AI "personalized alerts on watchlists + portfolios" reads on '965 E2/E3/E4 directly — and Webull's own SEC 20-F admits event-contract litigation exposure.

(1) Vega product page (webull.com/vega): "real-time, personalized analysis and alerts based on each client's watchlists and portfolios" + "surfaces potential trades based on volume spikes or price anomalies" = LITERAL E2 profile + E3 filter-to-recommended-wager + E4 push-to-mobile. (2) 1.2M weekly active users + 10M+ queries/week (Stocktwits Q1 2026) = commercial-scale AI-recommender deployed. (3) FY2025 20-F (SOX §302/906 · Denier + Wang · Apr 9, 2026): "Event contracts, whether offered by Kalshi or others… resulted in litigation that we are party to" — SEC-sworn litigation admission forecloses Rule 12(b)(6) premature-infringement defense. (4) 162M prediction contracts in 2025 (81M in December alone); FY25 revenue $571M (+46%). (5) Denier Jan 27, 2026 Super Bowl $0-commission PR: "prices reflect probabilities" — CEO Markman-dispositive admission that event-contract prices encode odds.

★ Branding-Collision

Genius Sports · NYSE: GENI

★ Branding-Collision

Genius Sports · NYSE: GENI

Genius brands its AI platform "Moment Engine" — verbatim title match to '161 patent "Exciting Moment Pre-Cognizant Notification."

(1) Q4 2025 earnings glossary (Mar 4, 2026): "Moment Engine: Genius Sports Limited's platform for embedding real-time sports data…." (2) CEO Locke on-call: "our moments engine now being externalized." (3) 20-F FY25: GeniusIQ "powered by an in-venue computer vision capture system." (4) BetVision Contextual Bet Prompts: "'Next Drive' markets presented during the fourth down" — LITERAL pre-cognizant push. (5) Genius's granted US 12,260,789 B2, Claim 1: "library of stored video sequences…semantic labels" — LITERAL '161 N1+N2. (6) Genius US 12,573,199 B2: "spatio-temporal index…indexes events at pixel locations" — '161 N2+N3+N4.

On-Chain Forensic

Polymarket · $20B+ val

Polymarket writes every accused trade to the public blockchain — we don't need discovery to prove infringement.

Polymarket's CTF Exchange contract (0x4bFb41d5B3570DeFd03C39a9A4D8dE6Bd8B8982E · Polygon) emits verbatim: event OrderFilled(bytes32 orderHash, address maker, address taker, uint256 makerAssetId, uint256 takerAssetId, uint256 makerAmountFilled, uint256 takerAmountFilled, uint256 fee). Every field maps to '965 E5: orderHash = registry entry, maker+taker = fractional ownership pair, makerAssetId = specific outcome token. Under FRE 902(13), auto-admissible — source verified on Polygonscan.

Verbatim Claim-Language

Smarkets BoT Exchange

Verbatim Claim-Language

Smarkets BoT Exchange

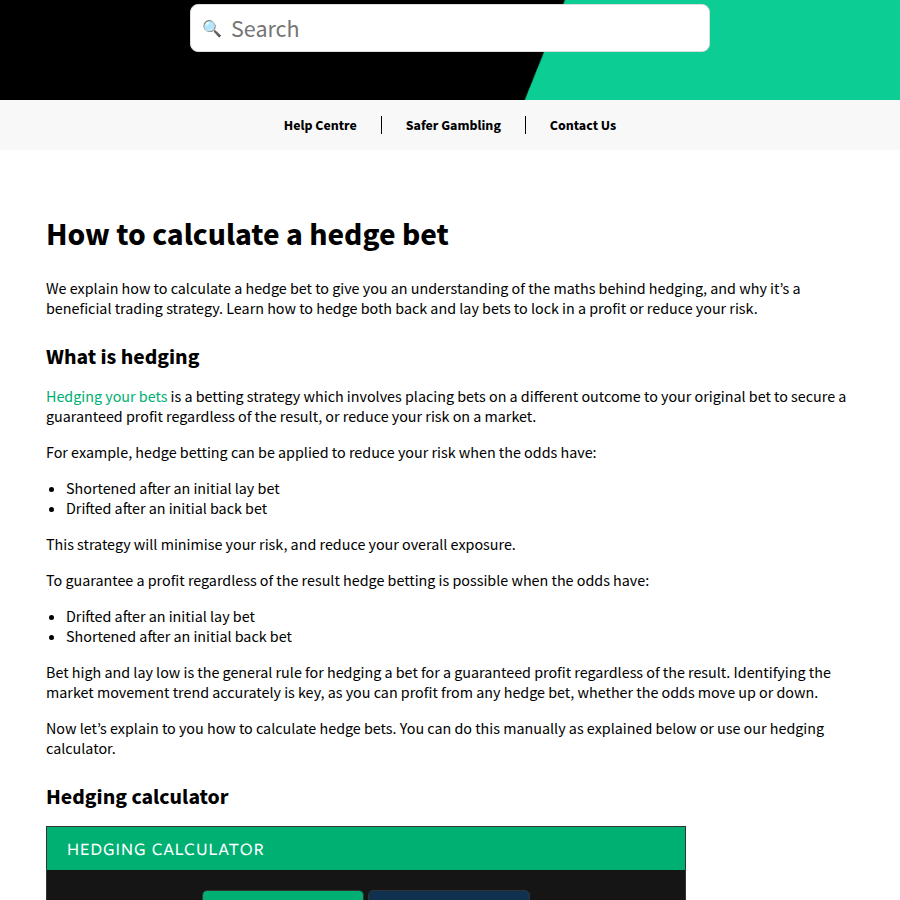

Smarkets' own Help Center uses Burillo's exact claim language — word for word.

Smarkets Help Center hedging calculator (public · live today): "lock in a profit regardless of the result… irrespective of the result." Burillo's Nov 30, 2020 USPTO statement — legally binding on both sides: "irrespective of contemporaneous odds" (filed to distinguish Pennock US 7,788,158).

| PATENT · CLAIM ELEMENT |

WagerWire

|

Kalshi

|

Polymarket

|

DraftKings

|

FanDuel

|

Robinhood

|

Genius

|

Fanatics

|

|---|---|---|---|---|---|---|---|---|

|

'965

Personalized Recommendation + Locked Odds

★ WagerWire leads

Others via platform suppliers

5 elements

|

||||||||

|

'965 E1

user profile

|

✓ ★ WW own App 17/938,040 Claim 1 · "ticket exchange system" |

✓ ★ Kalshi Rulebook + iOS "Product Personalization" |

✓ ★ on-chain wallet + tx history |

✓ ★ DK patent US 11,604,569 Claim 1 |

✓ ★ PredictsEmbeddedWebView chunk + How-to-Trade |

✓ ★ RH 10-K line 1808 · "agent facilitating" |

— B2B · § 271(b) |

✓ ★ CDNA Customer Account + iOS geolocation |

|

'965 E2

personalized filter

|

✓ ★ Dotan "signaling system" + sportsbook sync |

✓ ★ iOS "Product Personalization" + "For you" |

✓ category filter |

✓ ★ DK 10-K "customize home screen" |

✓ ★ Todisco + FD Ltd 19/410,345 "favorite teams" |

✓ ★ Cortex Digests · "analyzes holdings" |

— B2B · § 271(b) |

✓ ★ Sport pills + geolocation + trade-history profile |

|

'965 E3

recommendation

|

✓ ★ 40 live listings + Zendesk "Suggested Prices" |

✓ ★ Maker/Taker help + is_taker API |

✓ featured markets + /holders API |

✓ ★ DK 10-K + Simplebet ML PR |

✓ ★ US 12,307,861 GRANTED + Picks P2P sunset + ParlayHub API |

✓ ★ Custom Combos RFQ + Sportico |

✓ BetVision AI recommender |

✓ ★ Morton St. Market Maker affiliate ToU |

|

'965 E4 ★

locked odds

|

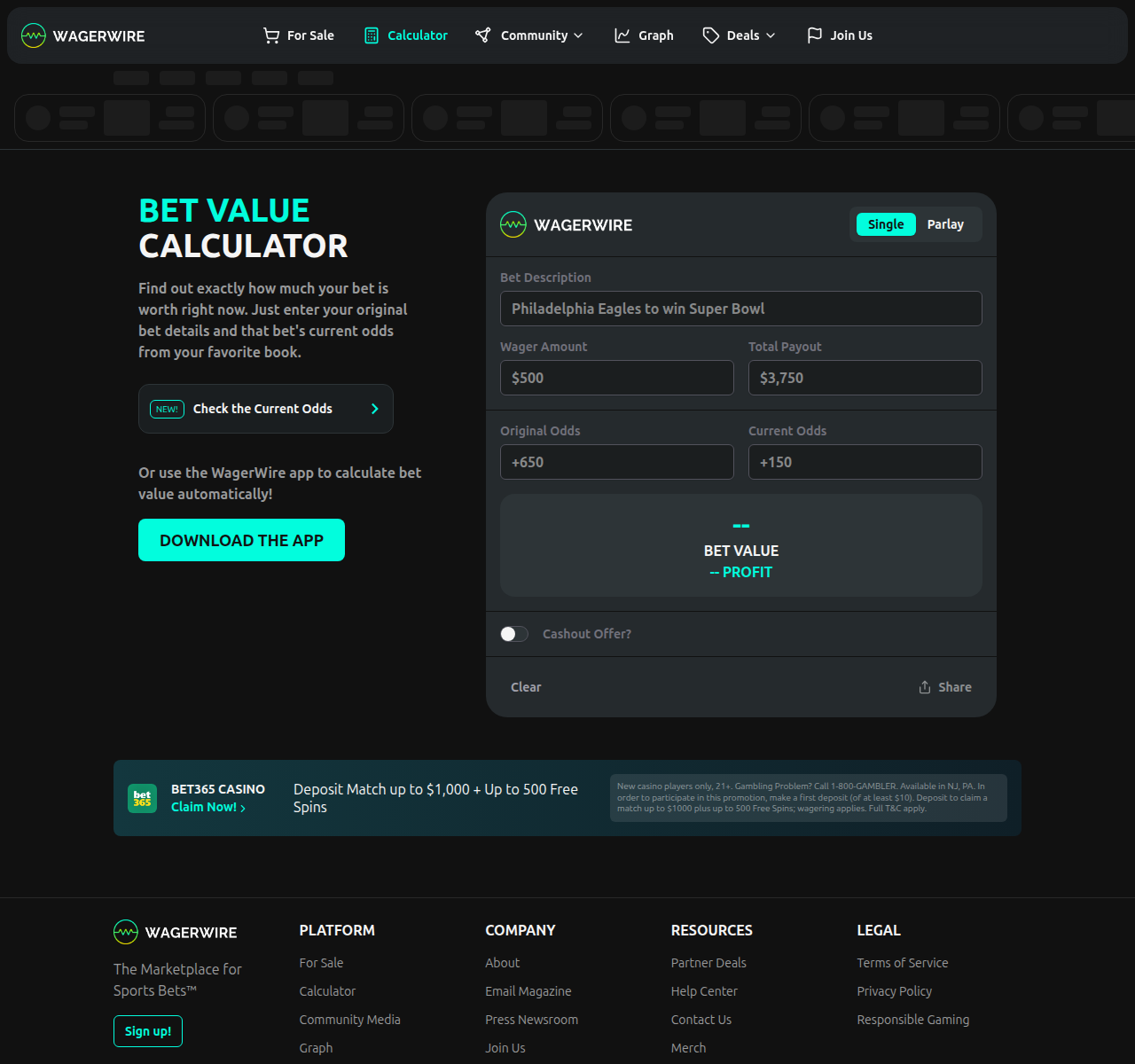

✓ ★★ GOLD · Calculator UI "Original"/"Current" |

✓ ★ Kalshi CFTC 13.1 (fractional lock) |

✓ ★ App Store "buy $0.67 · cash $1" |

✓ ★ Robins Q4 letter + trade-slip UI |

✓ ★ CME PR "$0.01–$0.99" + Predicts FAQ |

✓ ★ RH Help Center quintet (5 admissions) |

— B2B · § 271(b) |

✓ ★ CDNA Rulebook "Opening Trade Value" / "Closing Trade Value" |

|

'965 E5

fractional registry

|

✓ ★ WW own Claim 2 · "first ledger" |

✓ ★ CFTC 13.1 CRO + subaccount 0-32 API |

✓ ★ Poly on-chain CTF Exchange |

✓ ★ App Store "Replace__Trade__ASO" |

✓ ★ OBP (Order Book Plus) chunk + Cash Out |

✓ ★ Help Center fractional + 12B FY25 |

— B2B · § 271(b) |

✓ ★ CDNA Rule 5.4 Customer position account |

|

'966

Aftermarket Pool-Import

★ WagerWire only — unique architecture

6 elements

|

||||||||

|

'966 E1

aftermarket subscribers

|

✓ ★ WW own Claim 1 "third user" + GLI-33 |

— internal market · no pool-import |

— internal market · no pool-import |

— internal market · no pool-import |

— internal market · no pool-import |

— internal market · no pool-import |

— B2B · no consumer aftermarket |

— internal market · no pool-import |

|

'966 E2 ★

pool-import (non-subscriber)

|

✓ ★★ GOLD · FantasyWire DFS Pool 3/28/25 LITERAL |

— no non-subscriber pool-import |

— no non-subscriber pool-import |

— no non-subscriber pool-import |

— no non-subscriber pool-import |

— no non-subscriber pool-import |

— B2B · no pool-import |

— no non-subscriber pool-import |

|

'966 E3

non-subscriber data extract

|

✓ ★ RT Sports API + pricing engine |

— internal market · no pool-import |

— internal market · no pool-import |

— internal market · no pool-import |

— internal market · no pool-import |

— internal market · no pool-import |

— B2B · no consumer aftermarket |

— internal market · no pool-import |

|

'966 E4

registry write

|

✓ ★ WW own Claim 2 · "first ledger" |

— internal market · no pool-import |

— internal market · no pool-import |

— internal market · no pool-import |

— internal market · no pool-import |

— internal market · no pool-import |

— B2B · no consumer aftermarket |

— internal market · no pool-import |

|

'966 E5

publish for aftermarket

|

✓ ★ WW own Claim 1 · "posting sale offer" |

— internal market · no pool-import |

— internal market · no pool-import |

— internal market · no pool-import |

— internal market · no pool-import |

— internal market · no pool-import |

— B2B · no consumer aftermarket |

— internal market · no pool-import |

|

'966 E6

fractional acquisition

|

✓ ★ WW own Claim 2 · "updating first ledger" |

— internal market · no pool-import |

— internal market · no pool-import |

— internal market · no pool-import |

— internal market · no pool-import |

— internal market · no pool-import |

— B2B · no consumer aftermarket |

— internal market · no pool-import |

|

'706

Heads-Up Display Overlay for Online Wagering

★ WagerWire leads (chat UI)

Others via platform suppliers (HUD tech)

HUD + chat

|

||||||||

|

'706

HUD overlay

|

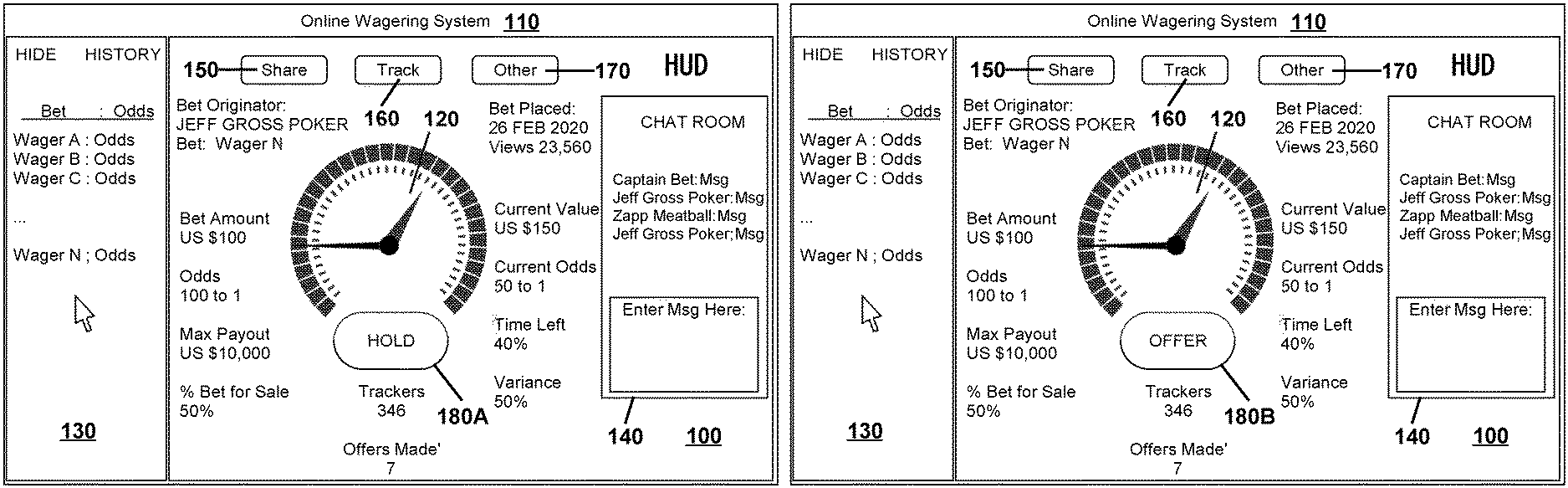

✓ ★★ GOLD · Sole direct · UNIQUE ACCEPT/COUNTER/REJECT P2P chat |

— Ideas = public forum · no P2P transactional chat |

— Comments public · no P2P transactional chat |

— No subscriber-to-subscriber chat (customer-support only) |

— No P2P chat · AceAI is AI-chat only |

— No chat UI architecture |

— B2B · no direct chat UI |

— No P2P chat (Squad Bets is group-selection, not chat) |

|

'161

Exciting-Moment Pre-Cognizant Push Notification

Direct hit · live-video operators

Genius supplies the AI

CNN + live video

|

||||||||

|

'161

CNN exciting-moment

|

— no live-video product |

— no live-video product |

✓ ★ DAZN stream "key moments" + LIVETRADE |

✓ ★ BetVision KB0010566 + Simplebet ML |

✓ ★ FD 19/410,345 verbatim CNN + Pulse "as action unfolds" |

— no live-video product |

✓ ★ 20-F GeniusIQ CNN + "Moment Engine" glossary |

✓ induced via BetVision (Genius) |

|

Coverage

|

3 / 4 '965 + '706 + '966 sole |

1 / 4 '965 direct · '706 fails chat UI |

2 / 4 direct '965 + '161 · '706 fails chat UI |

2 / 4 direct '965 + '161 · '706 fails chat UI |

2 / 4 direct '965 + '161 · '706 fails chat UI |

1 / 4 '965 direct · '706 fails chat UI |

1 / 4 direct '161 · § 271(b) '965 Sportradar-class |

2 / 4 direct '965 + '161 · '706 fails chat UI |

Replace__Trade__ASO — DK marketing characterizes the product as "Trading" · apps.apple.com/…/draftkings-predictions